The biggest challenge for NBFCs and fintech lenders in 2026 is no longer generating leads—it is converting loan applications into approved and disbursed loans. Most lenders today lose between 35% to 70% of applicants before completion because of slow onboarding, complex forms, manual verification, poor mobile experience, delayed approvals, and repeated documentation requests.

A modern Loan Origination System (LOS) can dramatically reduce loan application drop-off rates and increase conversion efficiency across the lending funnel. Platforms like Roopya help lenders automate onboarding, KYC, underwriting, fraud checks, and decisioning to create a seamless borrower journey. Modern digital lending infrastructure enables NBFCs to reduce abandonment rates below 20% while improving approval speed, compliance, and portfolio quality.

What Is Loan Application Drop-Off?

Loan application drop-off refers to borrowers abandoning the loan process before submission, approval, or disbursement.

This typically happens during:

- Registration

- KYC verification

- Document upload

- Bank statement submission

- Credit evaluation

- eSign process

- Repayment mandate setup

If 10,000 users start a loan application and only 2,500 complete it, your drop-off rate is 75%.

In digital lending, every abandoned application means:

- Lost revenue

- Higher acquisition cost

- Lower approval efficiency

- Poor customer experience

- Reduced scalability

For NBFCs spending heavily on Google Ads, Meta Ads, affiliate traffic, or DSA networks, high drop-offs can destroy profitability.

Why Most NBFCs Have High Application Drop-Off Rates

1. Long Application Forms

Borrowers hate filling 10–15 page forms.

Traditional LOS systems ask for excessive information upfront, including:

- Personal details

- Employment data

- Income details

- References

- Banking information

- Address proof

- Manual uploads

Modern borrowers expect quick onboarding in under 5 minutes.

2. Poor Mobile Experience

More than 80% of Indian borrowers now apply through mobile devices.

If your LOS is not mobile-optimized, users abandon quickly because of:

- Slow loading

- Broken layouts

- Difficult document uploads

- OTP failures

- Unresponsive interfaces

3. Manual KYC Verification

Manual KYC creates friction and delays.

Borrowers today expect instant:

- Aadhaar verification

- PAN validation

- Face match

- CKYC lookup

- Bank verification

Modern LOS platforms automate these processes in seconds.

4. Slow Approval Turnaround

The longer the approval time, the higher the abandonment rate.

If borrowers wait:

- 24 hours

- 2 days

- 5 days

they often move to competing lenders offering instant approvals.

Digital-first lenders using AI-based underwriting approve loans within minutes.

5. Repeated Document Requests

Borrowers become frustrated when lenders repeatedly ask for:

- Salary slips

- PAN

- Aadhaar

- Bank statements

- Selfies

A modern LOS uses OCR and automated extraction to minimize manual uploads.

What Is a Modern Loan Origination System (LOS)?

A Loan Origination System (LOS) is software that automates the complete pre-disbursement lending journey.

It handles:

- Loan applications

- Borrower onboarding

- KYC verification

- Credit checks

- Fraud detection

- Underwriting

- Approval workflows

- Digital agreements

- eSign

- Loan disbursement

Modern LOS platforms use:

- AI automation

- API integrations

- Mobile-first workflows

- Real-time decisioning

- Digital verification systems

Platforms such as Roopya LOS Solutions provide end-to-end automation for Indian NBFCs and fintech lenders.

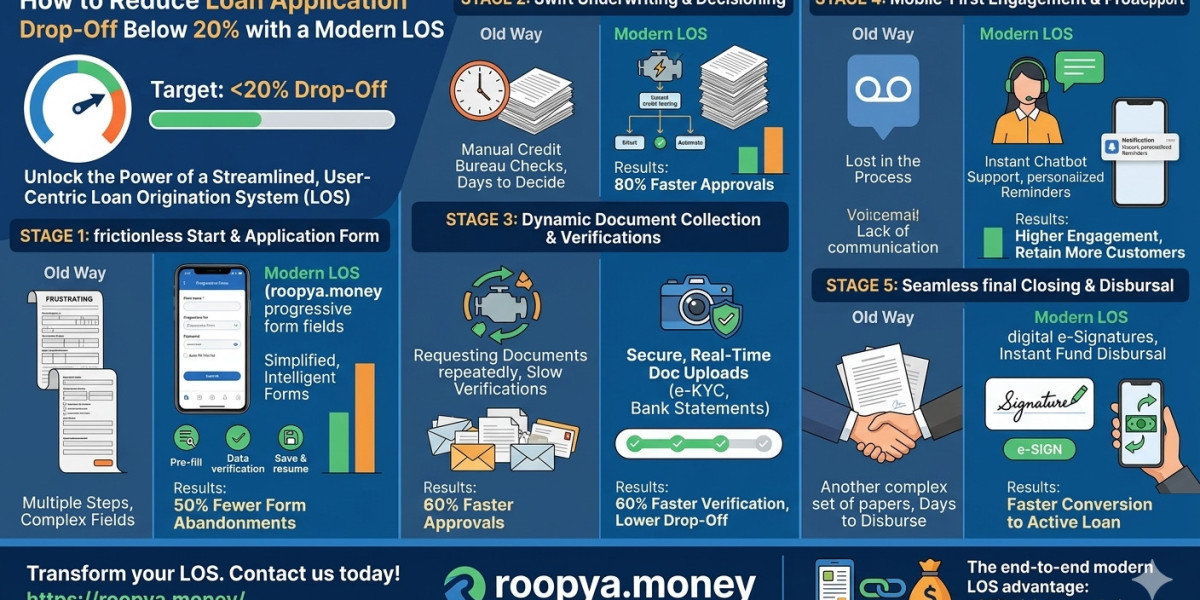

How a Modern LOS Reduces Loan Application Drop-Off

1. One-Click Digital Onboarding

Modern LOS platforms reduce friction with:

- Pre-filled forms

- Aadhaar-based auto-fetch

- Mobile OTP verification

- PAN auto-validation

- API-driven customer profiling

Instead of asking users to manually fill lengthy forms, the LOS auto-populates customer information instantly.

This reduces onboarding time from 20 minutes to under 3 minutes.

2. Automated KYC & eKYC

Modern LOS systems integrate directly with:

- Aadhaar eKYC

- PAN APIs

- CKYC

- DigiLocker

- Face verification

- Liveness detection

This removes manual review bottlenecks.

According to modern digital lending platforms, automated KYC can reduce onboarding abandonment significantly while improving fraud prevention.

3. AI-Based Credit Decisioning

Traditional underwriting is slow.

Modern LOS platforms use AI and rule engines to evaluate:

- Bureau score

- Bank statements

- Cash flow

- Income patterns

- Existing obligations

- Fraud signals

AI-based decisioning reduces approval time from days to minutes.

This creates:

- Faster approvals

- Better customer satisfaction

- Higher loan conversion rates

4. Smart Document OCR

Modern LOS platforms use OCR to automatically extract information from:

- PAN cards

- Aadhaar cards

- Salary slips

- GST certificates

- ITR documents

- Bank statements

Instead of manual typing, borrowers simply upload documents through mobile cameras.

This reduces friction dramatically.

5. Mobile-First Borrower Experience

Modern LOS systems are designed primarily for smartphones.

Features include:

- Progressive application forms

- App-based onboarding

- WhatsApp integration

- Camera-based uploads

- Real-time status tracking

- Instant notifications

Mobile-first lending experiences significantly reduce abandonment rates.

6. Instant Eligibility Checks

Borrowers abandon applications when they are unsure whether they qualify.

Modern LOS platforms instantly evaluate:

- Income eligibility

- Credit score thresholds

- FOIR

- Loan limits

- Risk categories

This prevents borrowers from wasting time on applications likely to be rejected.

7. Real-Time Progress Tracking

Borrowers want transparency.

Modern LOS dashboards show:

- Application progress

- Pending steps

- Verification status

- Approval timelines

- Disbursement updates

This keeps users engaged throughout the process.

8. Digital Agreements & eSign

Traditional physical agreements create huge drop-offs.

Modern LOS systems automate:

- Loan agreement generation

- eStamping

- Aadhaar eSign

- Digital consent capture

Borrowers can complete everything digitally in minutes.

9. Automated Communication Workflows

Many applications drop because lenders fail to follow up.

Modern LOS platforms automate:

- SMS reminders

- WhatsApp nudges

- Email notifications

- Application recovery campaigns

- Pending document alerts

Automated engagement workflows bring users back into the funnel.

Key Metrics to Track Loan Application Drop-Off

To reduce abandonment below 20%, lenders must track funnel analytics carefully.

Important LOS Funnel Metrics

| Funnel Stage | Key Metric |

|---|---|

| Registration | Signup completion rate |

| KYC | KYC success percentage |

| Document Upload | Upload abandonment |

| Underwriting | Approval turnaround time |

| eSign | Agreement completion rate |

| Disbursement | Final conversion rate |

Modern LOS analytics dashboards help lenders identify where borrowers exit the funnel.

Ideal Loan Funnel Benchmarks in 2026

Traditional Lending Funnel

| Stage | Conversion |

|---|---|

| Application Started | 100% |

| KYC Completed | 65% |

| Documents Uploaded | 50% |

| Approved | 35% |

| Disbursed | 25% |

Drop-off = 75%

Modern LOS Funnel

| Stage | Conversion |

|---|---|

| Application Started | 100% |

| KYC Completed | 90% |

| Documents Uploaded | 82% |

| Approved | 70% |

| Disbursed | 60%+ |

Drop-off below 20–40%

Best-in-class lenders now achieve under 20% abandonment using AI-driven digital onboarding systems.

Features Your LOS Must Have to Reduce Drop-Off

1. API-Based KYC

Must support:

- Aadhaar

- PAN

- CKYC

- DigiLocker

2. AI Fraud Detection

Should detect:

- Fake identities

- Device spoofing

- Duplicate applications

- Income fraud

Modern platforms now use multi-layer fraud engines.

3. Bank Statement Analyzer

Automated BSA improves approval speed and underwriting accuracy.

4. No-Code Workflow Engine

NBFCs should configure workflows without developers.

Modern no-code LOS systems allow rapid product changes and policy updates.

5. Multi-Channel Origination

Applications should work through:

- Mobile apps

- Websites

- APIs

- DSAs

- Co-lending partners

6. AI Credit Rules Engine

Automated decisioning is critical for scaling.

7. Real-Time Analytics Dashboard

Your LOS should track:

- Funnel conversion

- Approval ratios

- Drop-off sources

- TAT performance

- Fraud rates

Best Practices to Reduce Loan Application Abandonment

Simplify Forms

Only ask essential information initially.

Collect additional data later if required.

Reduce Steps

Aim for:

- 3–5 onboarding screens

- Single-page mobile journey

- One-click uploads

Improve Page Speed

Slow pages increase abandonment significantly.

Modern cloud LOS systems improve performance and scalability.

Use Progressive Data Collection

Do not overwhelm users upfront.

Collect information gradually.

Enable Resume Applications

Borrowers should continue applications later without restarting.

Use WhatsApp Integration

WhatsApp reminders improve completion rates.

Offer Instant Status Updates

Real-time updates increase trust and engagement.

Minimize Manual Review

Automation reduces delays and customer frustration.

Role of AI in Reducing LOS Drop-Off

AI is becoming central to digital lending.

Modern AI-driven LOS platforms help lenders:

- Predict abandonment risk

- Trigger automated recovery workflows

- Personalize borrower journeys

- Detect fraud instantly

- Improve approval accuracy

- Reduce underwriting TAT

Platforms using AI underwriting report much faster approvals and improved operational efficiency.

Why Indian NBFCs Need Modern LOS Platforms

India’s lending ecosystem is changing rapidly because of:

- RBI compliance requirements

- Digital borrower expectations

- UPI adoption

- Account Aggregator ecosystem

- Embedded finance growth

- Co-lending expansion

Legacy systems cannot support modern lending scale.

Digital LOS platforms are now essential infrastructure for:

- NBFCs

- Fintechs

- Microfinance institutions

- Gold loan companies

- MSME lenders

- Consumer finance companies

How Roopya Helps Reduce Loan Application Drop-Off

Roopya Digital Lending Platform offers a modern AI-powered LOS designed specifically for Indian lenders.

Key capabilities include:

- Digital onboarding

- Aadhaar eKYC

- PAN verification

- OCR automation

- AI underwriting

- Fraud detection

- Real-time decisioning

- No-code workflows

- Multi-bureau integrations

- LMS + LOS integration

- Collections automation

According to Roopya’s platform documentation, lenders can launch digital loan journeys in days instead of months while automating major lending operations.

Future of Loan Origination Systems in 2026

The future of LOS technology includes:

Hyper-Personalized Lending

AI-driven borrower journeys based on customer profiles.

Embedded Lending

Loans integrated directly into:

- Ecommerce

- B2B platforms

- SaaS products

- Payments ecosystems

Real-Time Risk Scoring

Dynamic credit models using:

- Banking data

- GST data

- Behavioral analytics

- Transaction history

Fully Automated Lending

End-to-end digital lending with minimal human intervention.

Reducing loan application drop-off below 20% is achievable only when lenders eliminate friction from the borrower journey. Traditional manual lending workflows are no longer sustainable in a digital-first financial ecosystem.

A modern Loan Origination System (LOS) enables lenders to:

- Automate onboarding

- Accelerate approvals

- Simplify KYC

- Improve mobile experience

- Reduce documentation friction

- Enhance fraud prevention

- Deliver instant customer experiences

For NBFCs and fintech lenders, the LOS is no longer just operational software—it is the core growth engine of digital lending.

Platforms such as combine LOS, LMS, analytics, AI underwriting, and collections into a unified lending infrastructure built for Indian financial institutions. By adopting a modern LOS, lenders can significantly improve conversion rates, reduce acquisition costs, and scale lending operations efficiently in 2026 and beyond.